Economic Outlook

Outlook Summary:

Slower growth through the remainder of 2022 that will continue to 2023

Inflation of approximately 4% during the first half of 2023

Stock market correction with occasional bear market rallies during the remaining of 2022

Gradual adjustment of housing prices back to the levels seen in early 2021 (depending on sub-markets, we might see double-digit drops). The correction will be followed by two or three years of minimal growth

Lessons from History:

“History doesn’t repeat itself, but it often rhymes” - Mark Twain

A series of unprecedented events during the past two years have created an environment of uncertainty in which any insignificant news creates a disproportionate response in the markets. With the equity and bond markets seesawing in the past few months, we’re dealing with issues such as heightened worries about recession, low consumer sentiments which have not impacted consumer spending, abundance of liquidity that is tightening, strong participation of retail investors in capital markets who are easily manipulated, move toward deglobalization, war, and future geopolitical risks. When we look into the past panics and manias, we see similar patterns but with varying intensity. Fear and greed have always been inherent in investing and this time is no different. However, the manifestations and the intensities are different, which makes the course of events and the outcome different each time. Because of the variations in the past events and also the fact that inevitably there will be some unexpected new development that will change the course of events (as it is each time), we don’t attempt to predict the future with certainty. Instead, our goal is to provide a roadmap based on available information and guided by the past events. In addition, we’d like to highlight the warnings signs and the known traps to prevent investors from making fatal mistakes. Below are a few points from the past that we believe are relevant to the current situation:

1. Bear market rallies: Crashes don’t happen overnight. After a bubble is formed, it takes time for the bubble to burst. Below is an example from the 1929 stock market crash.

Source: Federal Reserve Board

As you can see, it took two years to get from point A (peak) to point D (trough). On its way down, there was a rally (i.e. bear market rally). At point B (around 200), based on the false expectations that the worst was behind, the stocks rallied up to 280. So, hypothetically, one could have a gain of 40% if bought at point B and sold at point C.

So when you hear commentators point out to bear market rally, it’s not some hypothetical concept. It’s real and might cause real financial damage.

Source: Wealth, War and Wisdom, Barton Biggs, Wiley Inc., 2008

2. During the time of utmost optimism, we frequently hear the phrase that ‘this time is different’ (or some variation of it). Having high conviction is not bad on its own. It’s the actions that follow. Usually, investors borrow excessively, which benefits them during rising markets, but will hurt exponentially when markets stagnate. This is usually the time when luck is confused with competence. The recent trends (which are positive) are extrapolated in perpetuity, and recency bias and confirmation bias are at all time highs. What exacerbates this situation is cheap money (low interest rates) and excessive money printing. US has been more immune from this given that USD is the reserve currency, but many countries have suffered over and over again.

3. Just because investors are panicking or are skeptical, it doesn’t mean that something is going to go wrong. By the same token, we should not just dismiss those who think, contrary to the popular belief, that the market will hold strong. A good example is post-WW2 era. Many investors at the time were making comparisons between then and WW1 and the American Civil War. In both cases (WW1 and the Civil War), we had economic slumps after the wars ended. However, as it turned out WW2 was different. Although wars are detrimental to the economies, they work their way into the economy through certain mechanisms, and if those mechanisms are impacted by other forces, then we won’t necessarily see the expected outcome. That was certainly the case after WW2, but it wasn’t the case with Vietnam War a couple of decades later.

Source: Wealth, War and Wisdom, Barton Biggs, Wiley Inc., 2008

4. US went through an inflationary period in the late 1960s. The Fed Chairman at the time (Arthur Burns) did not respond appropriately and decisively which resulted in an out-of-control inflation that ran for a decade. To curb inflation, the next Fed Chairman Paul Volcker tightened the monetary policy (increased the rates) and caused a recession and high unemployment in order to destroy demand, which worked effectively. Once inflation came under control, a decade of economic growth and prosperity followed. Please note that high unemployment resulted in demonstrations and social unrest.

Where are we now?

High inflation: we are experiencing high inflation. Headline inflation is at 8.5% (latest release: July 2022) which is 0.6% lower than last month, but still much higher than the target of 2%. Note that 2% is not based on research. It’s just a target that by experience has worked well in the past.

GDP: The US has had two negative consecutive GDP prints in Q1 and Q2-2022. Many call it a ‘technical recession’ because they believe we’re not actually in a recession. What is a recession? As defined by the National Bureau of Economic Research (NBER), a recession involves “a significant decline in economic activity that is spread across the economy and lasts more than a few months.” This is otherwise referred to as the three Ds: Depth, Diffusion, and Duration.

In our view, although the economic activity declined, the economic position of consumers is strong. In other words, consumers have a strong personal balance sheet with savings in the bank account and recent wage increases. As it relates to corporations, we can categorize them into two groups: 1) corporations with sound business models and strong growth plans; and 2) zombie corporations, whose sole existence is because of the abundance of cheap money. We believe that a recession is necessary to clean the economy from zombie corporations. The first group, just like consumers, is in a good financial position. Therefore, there is no sign of distress when it comes to consumers and corporations (group 1, as defined above).

Consumer sentiment is low, but the recent survey showed a slight improvement in the month of July.

Unemployment is at a record low. The latest jobless claim does not show a significant change month-over-moth and the date indicates that those who are losing their jobs are able to find a new job reasonably quickly.

The Federal Reserve has responded to high inflation by raising the policy rate to a range of 2.5/2.75%. The Fed noted that they will not provide forward guidance as they used to and will be data-dependant. This has caused some uncertainty in the market because now everyone tries to guess what Fed’s reaction to the new information will be and formulate an investment strategy based on that.

Full capitulation has not happened yet. There are still investors with cash sitting on the sidelines waiting to deploy capital. This doesn’t necessarily mean that prices will go lower. It just means that there is a lot of cash to be deployed.

Statistics from Mastercard and Visa indicate that credit spending is high and the balances are increasing.

The Wealth effect is still high. In other words, following the rise of the property and stock values in recent years, households feel richer and they spend more (even though it’s on paper and is unrealized). Given that the current inflation is driven by a mismatch between supply and demand, this wealth effect exacerbates inflationary forces.

The housing market is cooling down but the rents are climbing higher. There are many projects that are awaiting to be completed in the coming year which will add to the inventory, but there is a significant supply shortage (approx. 1 year of construction by some expert estimates) to even out the supply and demand.

Stock markets experienced a correction around June but it has recovered around 15% from the lows but not as high as it was in Jan 2022.

Future Outlook

Inflation: Our base case is that inflation will remain high. When we look at the details of the CPI publications, some prices are up while others are not. The same choppiness exists in wages. As the impact of price increases permeates through different parts of the economy, we see a process that is impacted by both economics and psychology. The initial reaction to higher prices, as evidenced by economies that experienced high inflation, is denial, as customers cut down on some expenses because they find the new prices outrageous. However, they gradually get used to it and the consumption increases more or less to the previous level. The higher spending will erode consumers’ savings which were built through COVID lockdown. For lower income, it’s funded by borrowing. The recent statistics show savings are impacted just slightly, but credit has expanded in recent months. As this is not sustainable, consumers will request for higher wages, in some instances forcefully by forming unions, organizing strikes, etc. This is the inflicting point. If the Fed continues with tight monetary policy, some companies cannot increase wages and will go bankrupt. This will definitely result in social unrest. Again, if the Fed does not blink, then we will see the inflation coming down to 3 to 4 percent around Q3-2023. Unfortunately, politics might disrupt this position. Any spending bill, although well-intended, increases the risk of flaring up inflation (due to misallocation of the funds, which is bound to happen).

Monetary Policy: The Fed’s mandate is to fight inflation and keep unemployment low (and promote financial stability). Unemployment and inflation are moving in opposite directions. They are usually within the acceptable range, but sometimes there is a conflict between the two. The situation we’re currently in is one of those times. When this happens, it appears that the right course of action is to fix inflation first, even if it’s in the expense of high unemployment. This is basically how we got out of the Great Inflation (70s). So, we believe that the Fed will increase the rates one more time in September by 75bps (less likely 50bps) with another hike in November.

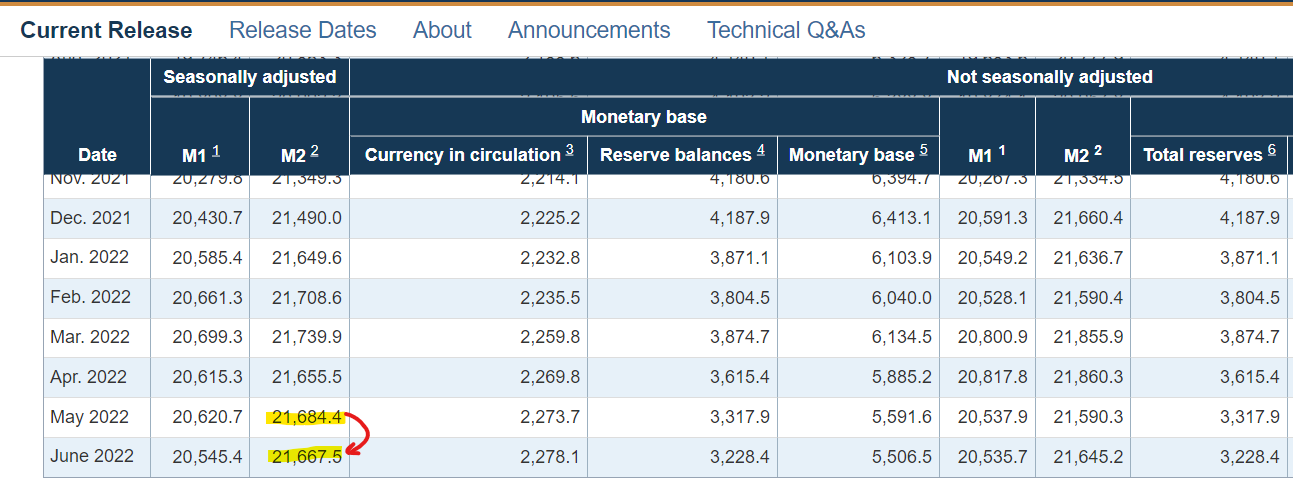

At the same time, one thing that is not talked about much but is running in the background is the Fed’s balance sheet, which they have indicated are planning to downsize. The way they will do is that they will let the financial assets they own now to expire and not to replace them (while they won’t actively sell them either). A big one is coming in September 2022. That will reduce the money supply and will work in conjunction with rate hikes (the two together is monetary tightening).

Below is the latest release that shows a meager reduction in June. But the larger reductions are coming soon.

Source: Federal Reserve

International investors: Currently, the US is comparatively the best place to invest. So, even if the US economy does not grow as much as projected, since it’s relatively better than the rest of the world, the money will be channeled to the US. Just one example is the heavy investment by Saudi’s sovereign fund in the US, as they are investing the excess cash due to higher oil prices in the US. This inflow of cash will keep the prices elevated.

Stock prices: We believe that there will be an adjustment to the stock prices during October to December time period when the impact of the high inflation and tighter monetary policy is felt. Depending on the geopolitics at the time, the economy can take a turn for a worse and we will see even lower stock prices in the first quarter of 2023. The leading indicator for this would be a sharp increase in the high yield spread, which has been compressed recently.

GDP: Our view is that in face of high inflation and the Fed’s Quantitative Tightening, the GDP will be under pressure, specifically during Q4-2022 and Q1-2023.

The housing market has shown signs of cooling. A mass completion of the projects is expected soon in the US, which will provide relief to the already tight market. But the US housing market is still significantly under-supplied. Combining that with the low sentiment among builders, we expect the current dynamic to continue. In terms of prices, we will expect a correction in the coming months specifically in the hot secondary markets. We acknowledge that consumer behavior has changed after COVID and there is more appreciation for larger places, but the prices in some secondary markets have gone too high that are not supported by the income.

Disclaimer:

Forecasting the future state of the economy is complex because there are many variables in play. Quite often, the actual course of events is different from what is projected. As such, please read this forecast, or any other forecast for that matter, with this point in mind. This post is the editor’s view based on the historical data as well as available data at the time of the post, on August 15, 2022.