NNN - National Retail Property

SUMMARY:

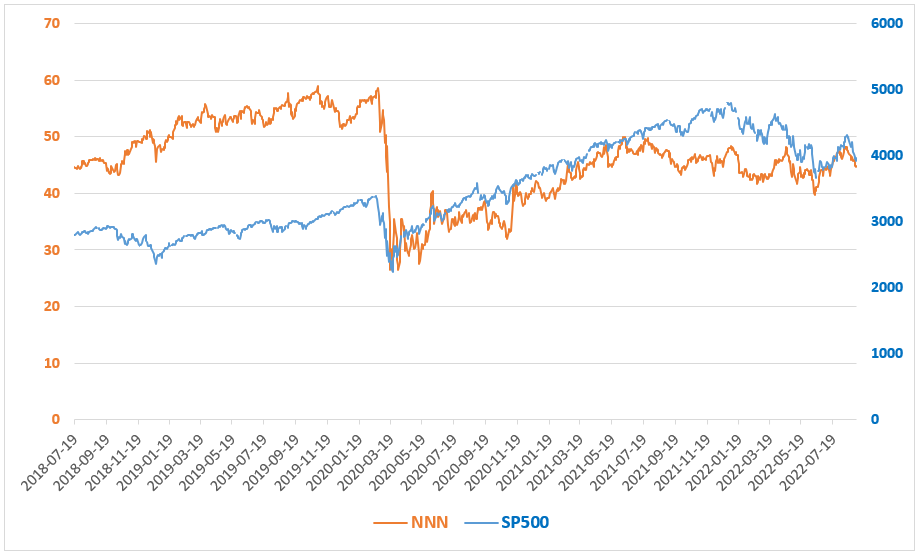

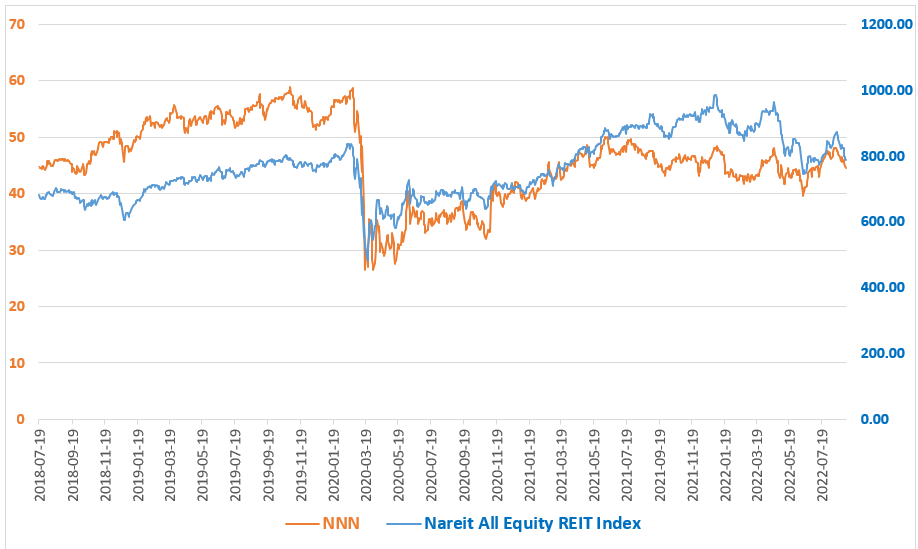

We believe that National Retail Properties (“NNN”) is fairly priced with our base case target price at $47.94. Our estimates for the bull and bear cases are at $49.64, and $44.17, respectively. We did not incorporate overly optimistic or pessimistic assumptions and they were in a close range.

NNN has stable operations with predictable and consistent cash flow:

The company owns, manages, and develops fee-standing properties which are diversified geographically as well as in terms of tenants’ line of trade.

Given the nature of the leases (net leases), the REIT is not significantly exposed to inflation, since the tenants are responsible for most of the expenses. In addition, most of the leases have favorable features such as CPI increase, step-up increase, and percentage rent, which will contribute to NOI increases.

Stable cash flow from operations and consistent dividend payments.

DISCUSSION

-

Fully integrated REIT, formed in 1984 and is listed on NYSE under the ticker symbol “NNN”.

As of June 30, 2022, NNN owned 3,305 properties with a GLA of 33,758,000 SF in 48 states. The properties are 99% leased with weighted average lease expiry (WALE) of 10.6 years.

The portfolio is diversified geographically and in terms of the tenants' line of trade -

NNN is in the business of investment in real estate with a focus on the retail sector, specifically free-standing properties that are leased to high-quality tenants under net lease (under the net lease, tenants are responsible for most of the operating and capital expenditures).

NNN’s market cap is approximately $8 billion with total assets valued at approximately $12 billion. The company has been able to pay stable dividends for more than two decades.

Most of the tenants operate in line of trades that are resistant to e-commerce. -

The CEO has been with the company for many years and has made a significant contribution to the growth of the company. Other members of the top management held position with the company for multiple years, which in our view is a positive aspect of this REIT.

The board of directors is comprised of a diverse group of accomplished professionals, most of which are independent members. The chairman of the board is also an independent member. -

NNN has a strong balance sheet, with a favorable debt-to-asset ratio.

Cash generated from the portfolio is stable due to creditworthy tenants, long-term leases, and diversification. Most of the leases contain one or more feature allowing gradual rent increases, such as CPI increase, step-up rent, or precentage rent. -

The prospect of growth is usually limited in REITs because REITs are required to pay out an amount equal to their taxable income as dividends. Therefore, the opportunity for reinvestment is limited.

Considering the above, retail properties have been under pressure for a long time mostly because of the threat of e-commerce. The data shows that the investment in retail real estate has been limited, resulting in continuing positive absorption. The surveys show that the base rent for quality retail properties has been increasing for the past four quarters and is expected to continue.

VALUATION METHODOLOGY

Using the information in 10K and 10Q we constructed an ‘equivalent portfolio’ in Argus. Market assumptions are based on the general market conditions and our expectations of inflation, interest rate, and rent growth.

Using forward four-quarter NOI and a cap rate of 6%, we estimated the value of properties if sold today. In addition, we used DCF which allowed us to incorporate longer-term assumptions, such as expected growth of the company, future interest rates, and exit cap rate.

Using Argus, we created bull and bear scenarios. The most important aspect of our scenario analysis was the exit cap rate. Some less impactful assumptions we changed in our scenario analysis were general vacancy, credit loss, and inflation.

Below are argus files:

Argus valuation report - PDF

Argus valuation report - Excel

Argus bull scenario - Excel

Argus bear scenario - Excel

SEE BELOW THE SUMMARY OF VALUE ESTIMATION, USING ARGUS INPUTS:

FINAL WORD

Based on our calculation, the company is fairly valued. This is actually good news because it speaks to the ability of management who has been able to communicate the value of the company properly to investors. Investors can benefit from the choppiness of the markets during the two months ahead to find a proper entry point. On the day of writing this report, the dividend yield increased to 5% due to the drop in prices. NNN has a secured source of cash flow and it doesn’t appear to be impacted by the economic slowdown.